Our goal here at Credible Operations, Inc. , NMLS Number 1681276, referred to as “Credibility” below, is to provide you with the tools and confidence you need to improve your financial position. Although we promote products from our lender partners who compensate us for our services, all opinions are our own.

Your credit score is an important factor when it comes to qualifying for a personal loan. Here’s why it matters and how to increase your score. (stock struggle)

Your credit score affects your ability to get a loan, how much you can borrow, the interest rates you are eligible for, and sometimes whether you qualify to rent an apartment.

when I was Apply for a personal loanHaving a good credit score can help you get the lowest interest rates available. Here are three reasons why you should improve your credit score before getting a personal loan.

Credibility makes it easy View pre-qualified personal loan rates From different lenders, all in one place.

1. You may get a lower interest rate

Your credit score is one of the most important factors that determine the interest rate you are eligible for when taking out a personal loan - or any type of loan. In general, the better your credit score, the better the interest rate you will qualify for because you are less risky in the eyes of the lender. and the Best interest rates They are usually reserved for borrowers with excellent credit.

The interest rate you get on a loan is important for several reasons. First, it affects the amount of your monthly payment. It also determines your costs in the long run, and a higher interest rate can cost you thousands of dollars more over the life of the loan than a lower interest rate.

2. Lenders are more likely to approve you for a loan

Your credit score will also help determine if you qualify for a personal loan at all. If your score is too low, this may indicate to the lender that you may not be able to make your loan payments.

Whether you’re applying for a personal loan, a mortgage, a car loan, or something else, the lender usually has the minimum credit score you need to qualify. Some lenders mention this minimum score on their websites, while others do not.

Visit Credibility for Compare personal loan rates From different lenders, without affecting your credit score.

3. You may be able to borrow more

Another reason why your credit score is so important when applying for a personal loan is that it can affect the amount you can borrow. The better your credit score, the more confident the lender will be that you will pay off your loan. In return, they may loan you a higher amount.

some Personal Loan Lenders Offers loans of up to $100,000, but higher loan amounts may be reserved for borrowers with excellent credit. while, Someone with poor credit You may only qualify to borrow a smaller amount.

But just because you qualify for a larger loan doesn’t necessarily mean you have to borrow the full amount. It is important to borrow only what you need so that you do not pay extra interest.

What constitutes a credit score?

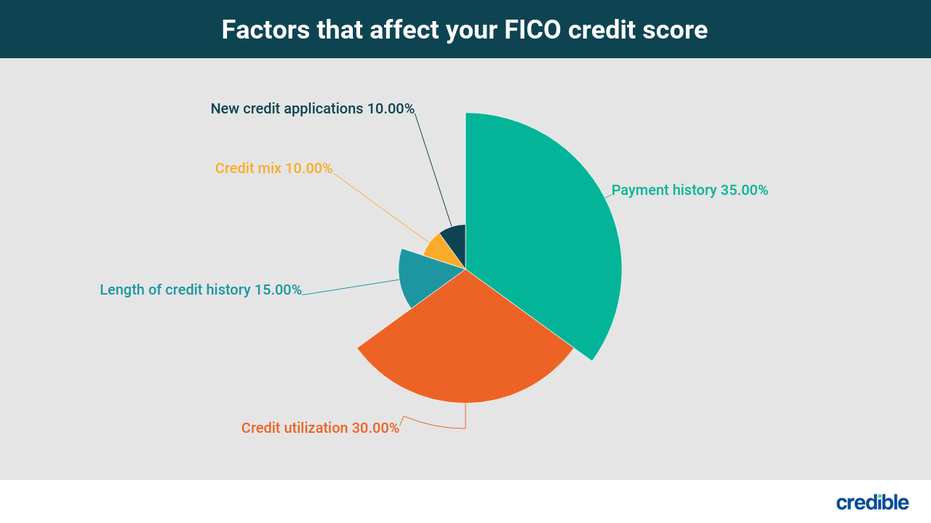

To increase your credit score to qualify for a personal loan, it is important that you understand the factors that affect your score. Your FICO score (which lenders use in the scoring form more) consists of five main categories.

- Payment date (35%) - Your payment history shows whether you have made loan and credit payments in the past. The better your payment history, the better your credit score. On the other hand, a late or missed payment can cause your credit score to drop.

- Credit use (30%) - Your credit usage indicates the percentage of available credit you are using. You can find it by dividing the amount of revolving credit you use by your total revolving credit limits. Lenders generally prefer your credit utilization to remain below 30%.

- Credit history length (15%) - This is the average age of your credit accounts, plus the age of your oldest and newest accounts. It also shows how long it’s been since you’ve used certain accounts.

- Credit mix (10%) - Your credit mix consists of the different types of credit in your accounts, including credit cards, lines of credit, and installment loans. You don’t need to have one of each type of credit, but having more than one type can be beneficial to your credit score.

- New Credit (10%) - The new balance refers to any new accounts you have opened. Opening multiple accounts in a short period of time can be a bad sign for lenders as it may indicate that you are struggling with managing your debt.

Ways to improve your credit

If your credit score isn’t quite where you want it to be, you can do several things to increase your score before you apply for a personal loan. Some of them may lead to quick results, while others take longer:

- Check your credit report. Checking your credit report can give you an idea of where you stand and what might make your score low, including missed payments. If you find errors on your credit report, you can dispute them with the appropriate credit bureau. Removing errors from your report can increase your score.

- Pay your bills on time. Your payment history is the single most important factor that determines your credit score, so it makes sense that simply paying your bills on time, every time, is the best way to increase your score in the long run.

- Pay off revolving debts. Credit card payments And other revolving debts can reduce your use of credit, which may increase your credit score.

- Increase your credit limits. In addition to reducing your debt to improve your credit utilization, you can also increase your credit limits. You may be able to do this by contacting your credit card company or requesting a raise through your online account.

- Avoid applying for new credit. Applying for new credit before applying for a personal loan can take a small hit in your credit score, potentially lowering your score temporarily by a few points.

If you are ready to apply for a personal loan, Credible makes it quick and easy Compare personal loan rates To find the one that best fits your needs.